Stable interest rates, tight supply – and new opportunities.

21.06.2026The Swiss National Bank is keeping its key interest rate at zero per cent, the supply of housing remains tight, and the regulatory burden in the construction sector continues to grow. The current environment in the Swiss property market combines favourable financing conditions with a structurally tight supply – a combination that keeps exclusive residential property in Switzerland attractive in the medium to long term, even as the first signs of a shift in interest rates appear on the horizon.

For buyers of exclusive residential property, this results in a remarkably stable yet selective environment – with attractive financing conditions but, on the other hand, a structurally limited supply.

The interest rate landscape: calm before the next move

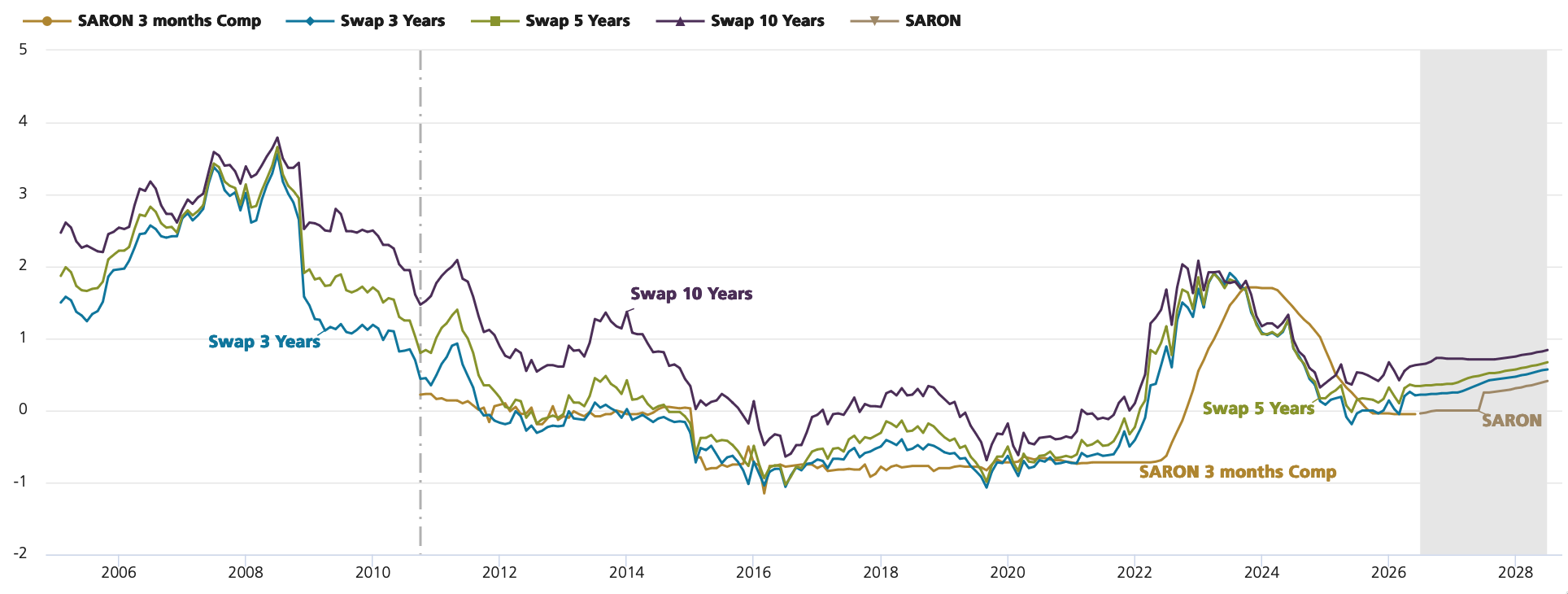

At its meeting on 18 June 2026, the SNB decided to keep the key interest rate at 0 per cent, following a series of interest rate cuts that began in 2024 and concluded in mid-2025. The key factors underpinning the continued expansionary monetary policy are the low level of inflation and a Swiss economy that is not expected to realise its full growth potential in 2026. You can read more about the implications of this decision for mortgage rates and the future trajectory of the Swiss National Bank’s key interest rate on the ‘Interest Rate Forecast and Trends’ web pages of UBS and Zürcher Kantonalbank.

For homebuyers, this means that financing conditions remain exceptionally favourable. The markets are already anticipating an SNB interest rate rise, which is why both government bond yields and mortgage rates are likely to remain at low levels for the time being – this also applies to SARON mortgages for the time being, although a certain rise in interest rates appears possible next year.

A turning point is nevertheless on the horizon: an economic recovery could begin in 2027, once the German fiscal stimulus takes effect and stronger momentum in the eurozone boosts Swiss exports – which is likely to prompt the SNB to raise its key interest rate from mid-2027 onwards. So, anyone wishing to secure favourable terms in the long term will – for the time being – find an attractive window of opportunity in the current environment, for example through a forward mortgage, which allows today’s terms to be fixed up to twelve months in advance.

Geopolitics as a new source of uncertainty

It is striking just how strongly geopolitical developments are currently influencing interest rate formation: at the start of May, yields on Swiss government bonds and mortgage rates rose against the backdrop of rising global inflation, but eased again in early June as hopes grew for a swift resolution to the Middle East conflict and a possible reopening of the Strait of Hormuz. Raiffeisen Switzerland also confirms this link in its study ‘Immobilien Schweiz Q2 2026’: rising energy prices resulting from the conflict in the Middle East are likely to affect construction costs and, consequently, rental price trends in the long term.

For owners of exclusive properties, this increased volatility serves as a reminder that financing strategies today need to be approached with greater flexibility than was the case just a few years ago – a combination of different maturities can pay off.

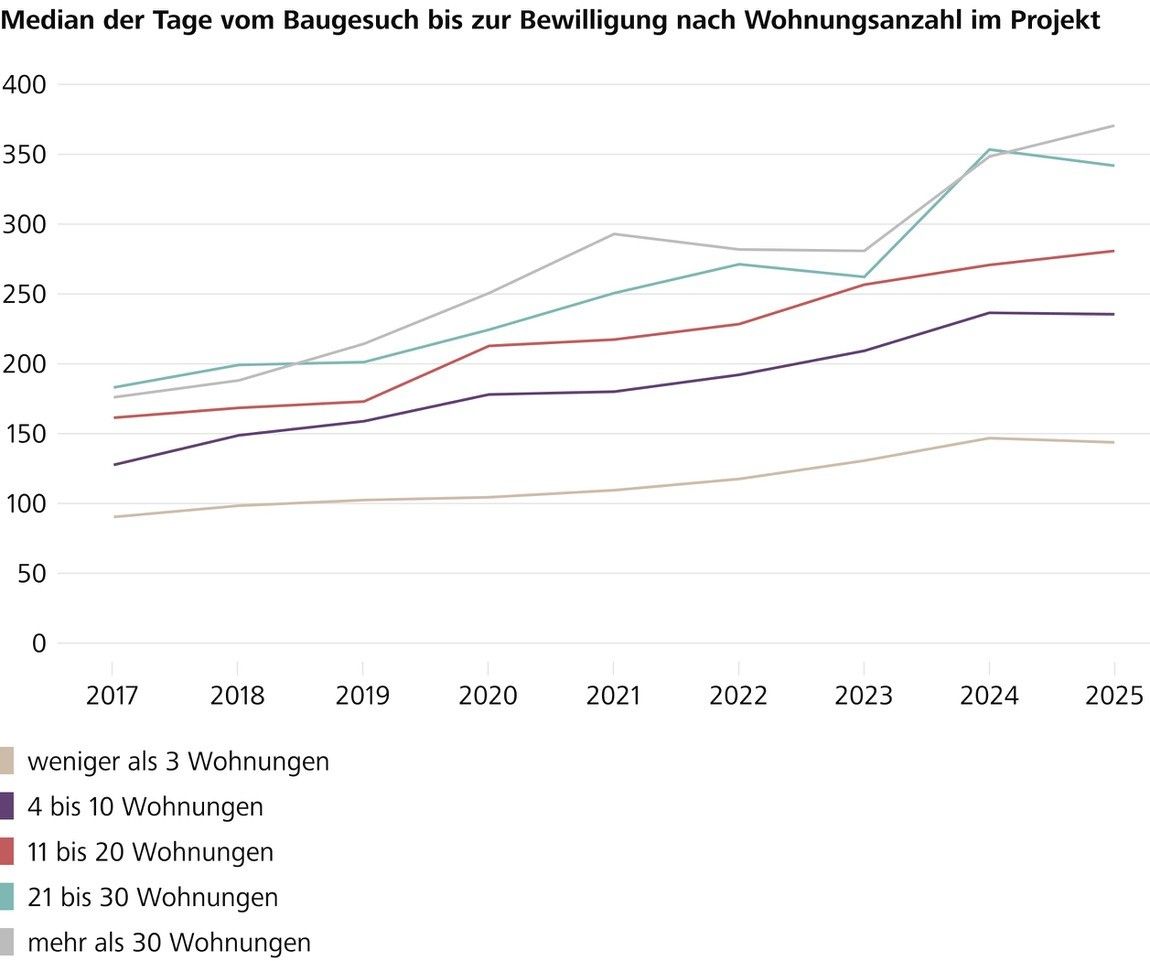

Supply remains tight – with noticeable consequences for upmarket locations

Whilst interest rates are favourable for buyers, the supply side is holding things back. Raiffeisen’s chief economist, Fredy Hasenmaile, attributes this primarily to increasing building regulations: The length of cantonal building laws has increased by an average of 26 per cent since 2005, and building regulations by as much as 32 per cent, whilst the number of unique legal terms – an indicator of the density of regulation – has risen by 10 to 15 per cent. Hasenmaile emphasises that, taken individually, each regulation often appears sensible, but taken together they increase the complexity, risks and costs of housing construction to such an extent that technical progress can no longer compensate for these effects.

The result: longer planning permission processes, higher planning risks and a level of construction activity that remains at a historically low level despite clear signs of a housing shortage. For the market in exclusive properties – already characterised by limited, often unique locations – this means a further tightening of supply, which further supports the value retention of existing premium properties.

The abolition of the imputed rental value: make use of the preparation period rather than wait and see

One issue that particularly affects homeowners is the abolition of the imputed rental value, which was approved by the people and the cantons in spring 2025. Eight months on, there has been hardly any reaction on the market – according to Hasenmaile, no increase in renovation activity has been observed so far, neither in renovation applications nor in the turnover of tradespeople.

As the reform will not take effect until the 2029 tax year, a strategic window of opportunity is opening up for owners of high-value properties: Renovations that are still tax-deductible today are particularly worthwhile if they are planned at an early stage. Hasenmaile expressly warns against waiting too long – not only because of the long lead times for many measures, but also because capacity bottlenecks are to be expected among tradespeople as soon as the anticipated renovation boom actually takes hold. Anyone who owns a prestigious property in need of renovation should therefore tackle the issue now – not wait until 2028.

What does this mean for buyers of exclusive residential property

Financing: Interest rates remain exceptionally favourable; anyone wishing to secure these terms in the long term should consider using forward mortgages or financing structures with staggered maturities before the expected interest rate turnaround in 2027 becomes a reality.

Supply shortages as a driver of value: The structural slowdown in new-build activity – exacerbated by growing regulatory complexity – means that particularly rare, well-connected premium locations are likely to maintain or further increase their value.

Seize the opportunity rather than let it slip by: Buyers are currently benefiting from a rare combination of low interest rates and (as yet) subdued market momentum in renovation projects – an environment that will change noticeably as we approach 2029.

What does this mean for property owners

Plan renovations now: The final years before the abolition of the notional rental value offer the best tax conditions for value-preserving investments – those who wait risk missing out on tax deductions as well as facing supply bottlenecks from tradespeople.

Property quality matters: In a market characterised by limited supply and rising regulatory hurdles for new builds, existing, high-quality properties are gaining relative importance – well-maintained properties are becoming a value driver in their own right.

Geopolitical vigilance: The recent interplay between the Middle East conflict, energy prices and interest rate trends demonstrates just how closely the domestic property market is now intertwined with global developments – a trend that will also influence future financing decisions.

Despite the limited availability of exclusive residential properties, we at Wüst und Wüst are pleased to assist you in finding your ideal home. On our property website, you will currently find a carefully selected portfolio of homes in the regions of Zurich, Zug, Lucerne, St. Moritz, Pfäffikon/SZ, and Basel.

Should you wish to sell your property, our experts will also support you with sound advice, in-depth market knowledge, and personal commitment.