SNB keeps key interest rate at zero: what does this mean for mortgages?

18.12.2025The Swiss National Bank (SNB) is leaving its key interest rate at zero per cent. For property owners, this sounds like stability. Nevertheless, some mortgage interest rates are rising. We explain why this is happening and what it means for the property market.

The current interest rate situation: stability with nuances

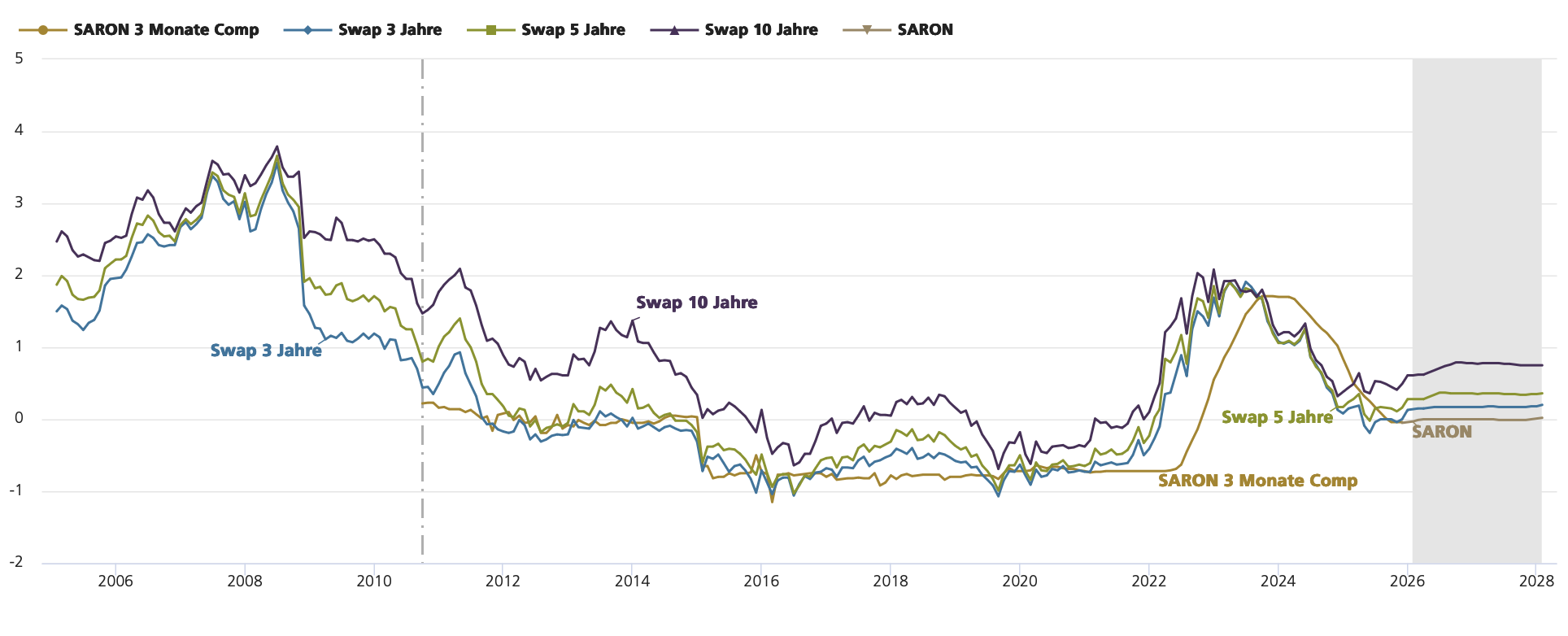

Wüst und Wüst closely monitors the financial markets, as they influence buying and selling decisions in the premium segment. A few days ago, the Swiss National Bank (SNB) decided, as expected, to keep the key interest rate at zero per cent. This is a welcome development for property owners. Nevertheless, interest rates have not fallen at some banks due to increased margins, and have even risen slightly for Saron mortgages.

UBS interest rate forecast: current situation and influencing factors

In its assessment of the current interest rate forecast, UBS writes: “Yields on Swiss government bonds and interest rates on fixed-rate mortgages have risen slightly since mid-November. The customs agreement between Switzerland and the US reduces the customs burden on Swiss exports to the US from 39 per cent to 15 per cent. This should reduce the risk of a significant economic slowdown and thus lower the probability of negative key interest rates from the Swiss National Bank.”

Very low inflation and below-average growth

Inflation of just 0.3 per cent is expected in 2026, but deflation is not anticipated. Our economy is likely to grow at a below-average rate of around 0.9 per cent in the new year. However, the customs agreement with the US is a ray of hope for the economy.

Interest rate hikes a long way off

The bank expects the SNB to continue this course in the new year; interest rate hikes are a long way off in Switzerland’s current economic environment. However, if the eurozone recovers thanks to Germany’s extensive fiscal package and the economic outlook for Switzerland brightens at the same time, government bond yields and mortgage interest rates could rise slightly next year.

Higher margins make mortgages more expensive

Despite the fall in key interest rates, which are now stable at zero per cent, homeowners have been faced with mortgage interest rates that are not falling or are slightly higher for several months now.

The banks cite three reasons for this:

- Stricter capital requirements due to ‘Basel III’

- Tighter regulation of minimum reserves

- Migration of debtors with low credit ratings to other institutions following the UBS-CS merger

These factors increase margins and make mortgages more expensive at some banks, including many cantonal banks.

It’s worth getting advice

With mortgage sums usually being high, even small percentage differences can generate a noticeable increase or decrease in costs. In addition to the possible terms and different interest rates offered by various providers, your own risk appetite also plays an important role when choosing a mortgage.

Those who can accept fluctuating interest rates may opt for the currently cheaper Saron mortgages, while fixed-rate mortgages guarantee longer-term budget security.

Our conclusion

The current interest rate situation remains stable, but bank margins are having a noticeable impact on mortgage interest rates. At Wüst und Wüst, we are your experts for the sale and marketing of exclusive residential property.

For financing questions, we work with trusted partners to give you access to reliable solutions — without offering financial advice ourselves. Our goal is to provide comprehensive support and the best possible advice to sellers and buyers. However, we do not offer financial advice ourselves.

Contact us now for a personal marketing consultation at any of our locations: Küsnacht/Zurich, Zug, Lucerne, St. Moritz and Pfäffikon/SZ.