Interest rates are rising: buy or wait?

01.06.2026The Swiss property market finds itself caught between a number of conflicting pressures: rising prices, increasing inflation and a structural shortage of supply. Anyone buying or selling now should be aware of the signs – particularly in the premium segment.

A market under pressure – but not in crisis

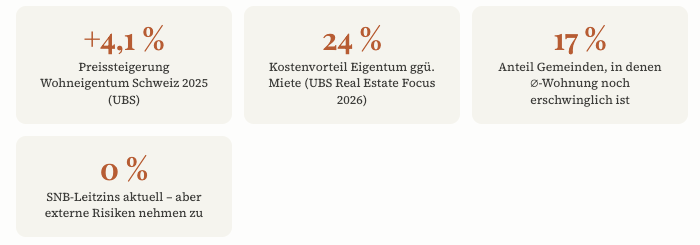

The Swiss residential property market finds itself in a peculiar state in 2026: robust, but strained. According to the latest UBS Real Estate Focus 2026, prices for flats rose by 4.8 per cent last year, whilst detached houses became 3.4 per cent more expensive. For the current year, UBS economists expect a slight cooling to around 3 to 3.5 per cent – a slowdown, but by no means a reversal of the trend.

At the same time, a geopolitical event has altered the broader context: the ongoing Iran conflict has driven up energy prices and global inflation expectations. As the NZZ (behind paywall) analyses, government bond yields have risen significantly – ten-year US Treasuries are yielding over 4.4 per cent, German Bunds around 2.9 per cent. Switzerland remains an island of stability at 0.36 per cent, yet fixed-rate mortgage rates in this country have already risen by more than 0.3 percentage points since February. The question of whether the SNB can maintain its key interest rate at zero per cent has become an open one.

For buyers: Getting on the property ladder has become more difficult – but it is still worth it

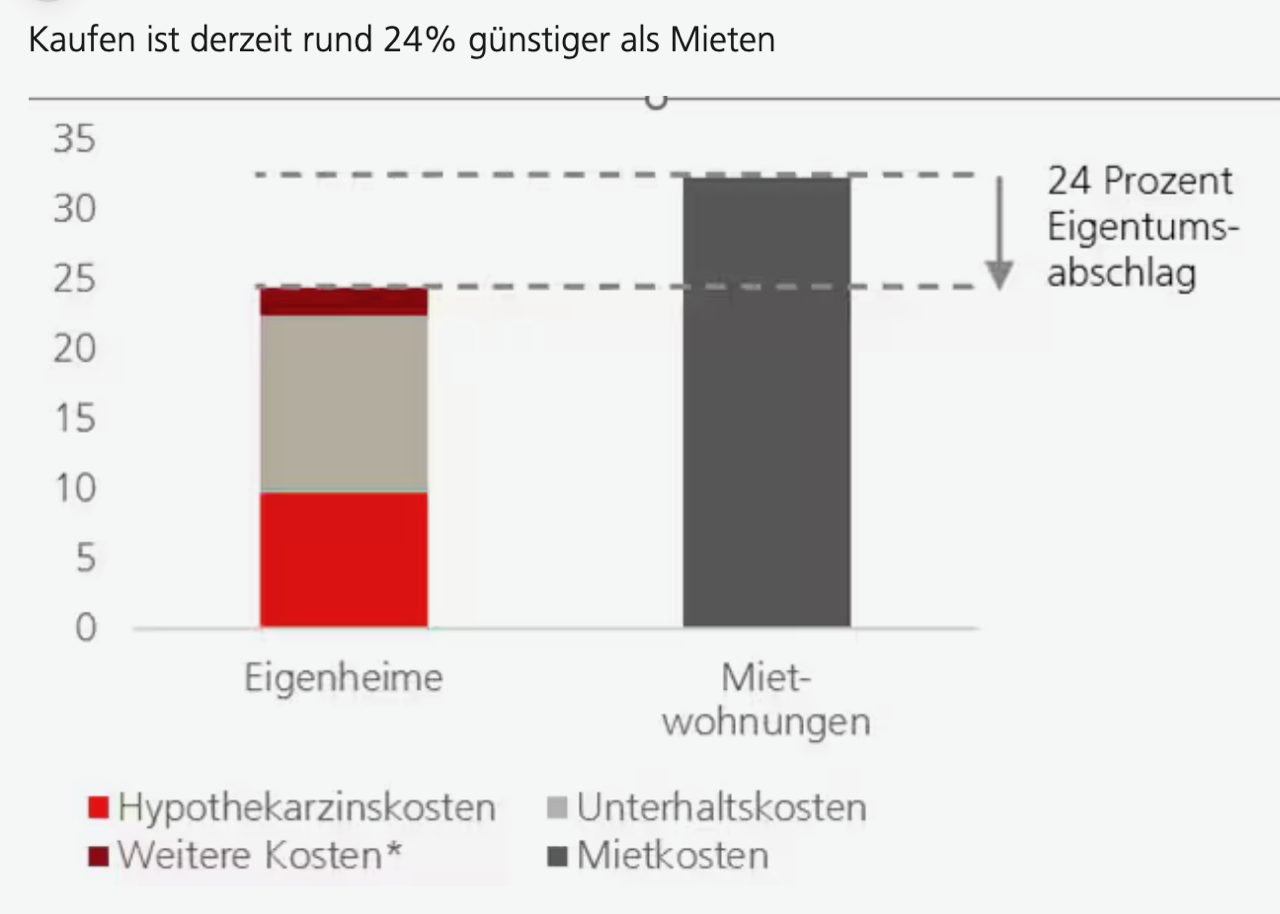

For prospective buyers in the premium segment, the situation is more nuanced. Although the running costs of a freehold flat are still around 24 per cent cheaper on average in Switzerland than the rent for a comparable property, thanks to comparatively low financing costs.

However, high entry prices are increasingly making affordability – that is, the ability to cover ongoing mortgage interest and repayments from one’s income – the key hurdle. Banks traditionally apply an imputed interest rate of five per cent, which pushes many households to their limits.

Opportunities for potential buyers:

- Long-term cost advantage over renting (approx. 24%)

- Stable value and wealth accumulation in the luxury segment

- Inflation protection: tangible assets retain purchasing power as inflation rises

- SARON mortgages remain attractive in the short term with stable SNB interest rates

- Exclusive locations hardly affected by increases in supply

Risks for potential buyers:

- Rising fixed-rate mortgage interest rates make financing more expensive

- Stricter affordability requirements from banks

- Geopolitical uncertainty may accelerate a shift in interest rates

- High equity requirements (min. 20% of market value)

- Price peaks in prime locations potentially vulnerable to correction if interest rates rise

UBS expert Claudio Saputelli, Head of Swiss & Global Real Estate, aptly sums up the key tension: prices have become so decoupled from average incomes that the banks’ affordability guidelines have become an insurmountable hurdle for many. In the premium segment, the opposite is true: Affluent buyers benefit from favourable financing conditions, but must expect their portfolios to be more sensitive to interest rate movements.

For sellers: Now is a strategically favourable moment

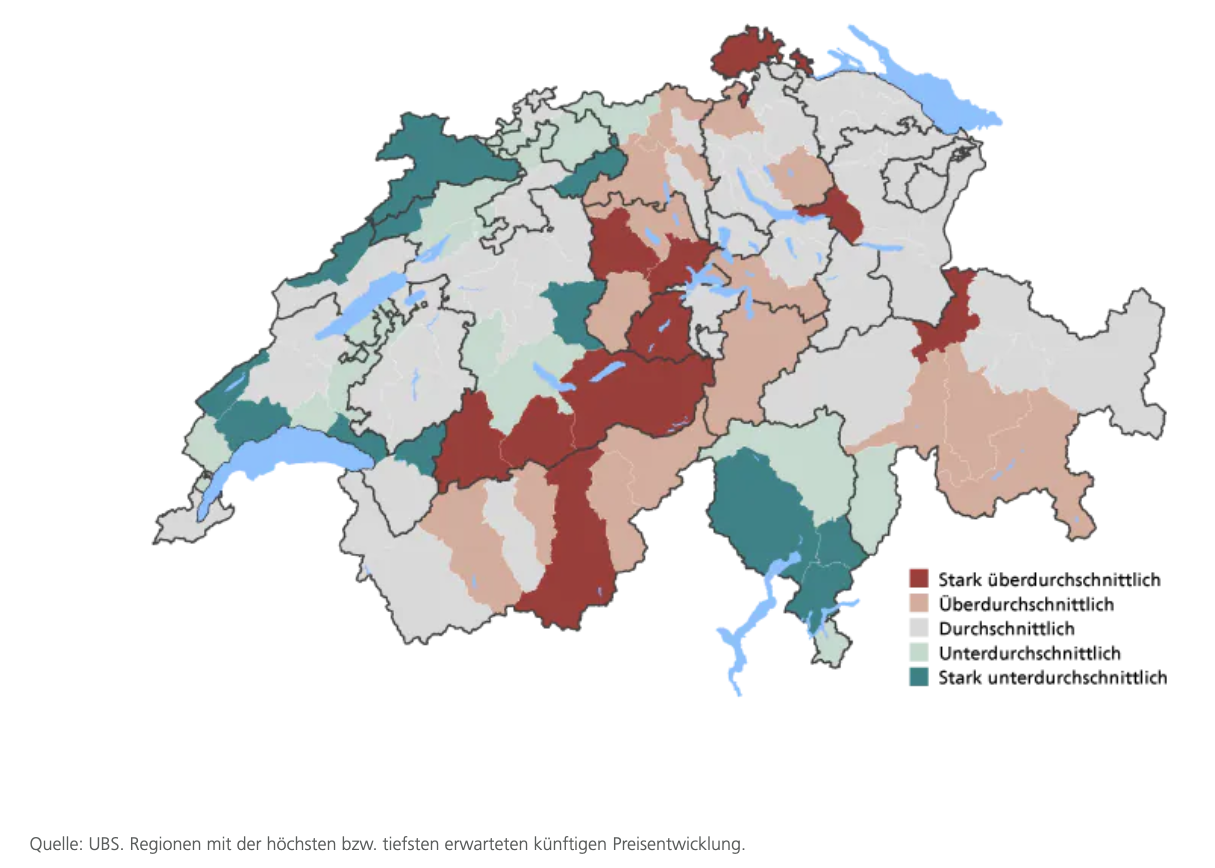

Anyone looking to sell a prime property today is acting from a position of strength. Supply remains structurally tight despite a slight increase in construction activity. Vacancy rates continue to fall, and demand for exclusive properties remains unbroken. In particular, the boom in renovation and conversion – the investment volume of such projects has almost doubled in five years, according to UBS – is driving prices in the upper segment even higher.

Opportunities for sellers:

- High price levels offer attractive sales proceeds

- Structural supply shortage strengthens negotiating position

- Renovation trend enhances the value of existing properties in the premium segment

- Demand from affluent buyers at home and abroad remains robust

- Selling early secures profits ahead of a possible interest rate rise

Risks for sellers:

- Rising interest rates could narrow the pool of buyers and create price pressure

- Significant capital gains tax on short-term holdings

- Existing mortgage must be discharged or transferred upon sale

- Economic uncertainty is dampening demand slightly

- Price softening in outlying areas is already visible

Mortgage strategy in times of rising inflation

According to the NZZ analysis, a shift is emerging in the fixed-rate mortgage market. As investors demand higher returns in light of the Iran conflict and rising inflation expectations, interest rates on fixed-rate mortgages have risen noticeably since the start of the year. The UBS economists expect a shift from variable SARON mortgages to fixed-rate mortgages to take place sooner than expected – a signal that homebuyers with a high level of debt, in particular, should take seriously.

For affluent buyers of exclusive properties, this means: Anyone taking out a five- or ten-year fixed-rate mortgage today is protecting themselves against further interest rate normalisation – but may be paying a risk premium for an event that has not yet materialised in Switzerland. The SNB has signalled that it will not raise its key interest rate in 2026. Yet banks’ margins on fixed-rate mortgages have already widened.

Exclusive locations: A segment of its own with its own rules

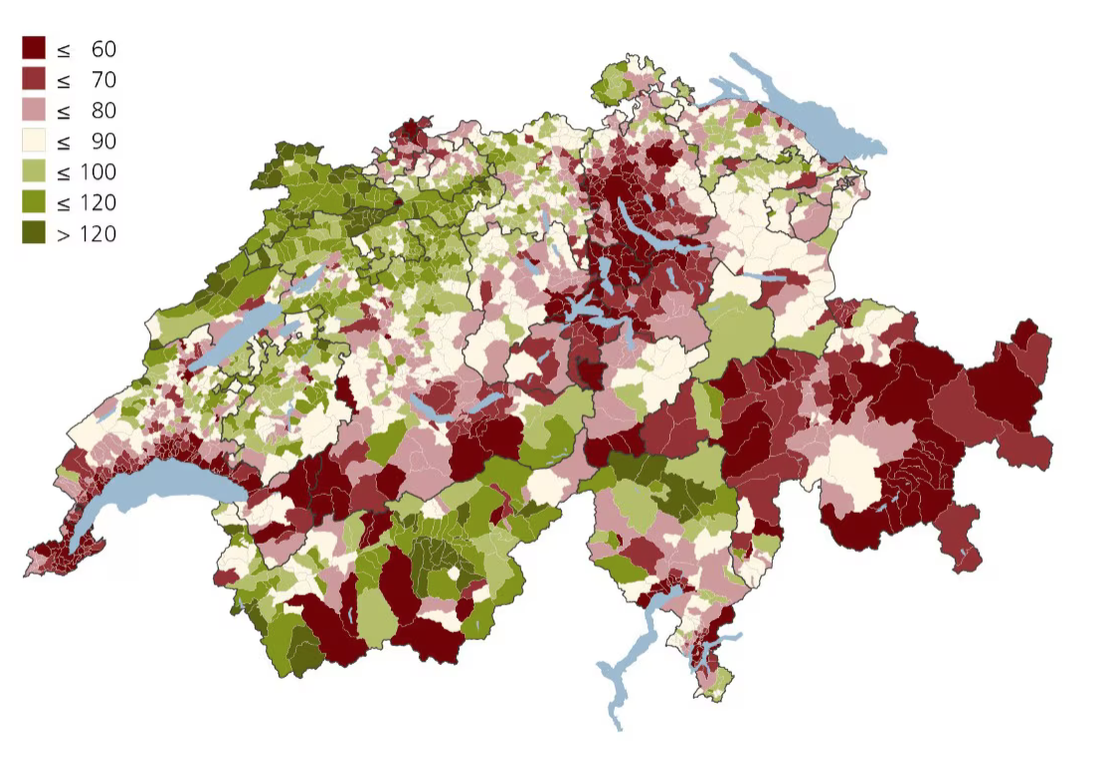

The premium segment operates by its own rules. Whilst affordable homes can now only be found in 17 per cent of all municipalities across much of Switzerland – primarily in the Jura, Valais and Thurgau – the luxury segment is benchmarked against international markets. Geneva, Zurich and the Grisons Lake District compete with London, Monaco and Lake Como. Here, affordability in the traditional sense plays a secondary role; instead, reputation, discretion and long-term value stability are the decisive factors.

It is particularly in this segment that tangible assets such as property tend to become more attractive during periods of inflation. Those holding liquid investments in bonds or money market products – according to the NZZ analysis (behind paywall), savings products often show a loss after adjusting for inflation – are seeking real alternatives. High-priced properties in exclusive locations serve not only as living space but also as capital investments with utility value.

Conclusion: Acting with foresight

The Swiss property market in 2026 offers compelling arguments for both buyers and sellers of exclusive properties – but no sure-fire success. Sellers benefit from a structurally tight market with stable demand and can realise profits at historically high levels. Buyers who carefully weigh up financial affordability and interest rate trends will continue to find a robust value proposition in prime locations – particularly if they wish to hedge against volatile inflationary pressures. The key factors remain: professional guidance, precise timing and a clear strategy for mortgage financing.

For advice on currently available exclusive properties, the team at Wüst und Wüst is always at your disposal.