Between a boom and hidden risks.

12.05.2026In spring 2026, the Swiss property market is more dynamic than it has been for a long time – record prices, historically low interest rates and sustained excess demand paint an enticing picture. Yet behind the glittering façade, political risks are mounting, and the era of effortless profits is drawing to a close. What this means for owners of exclusive properties – and why strategic action is needed now more than ever.

Prices on a record-breaking course – a boom that is surpassing itself

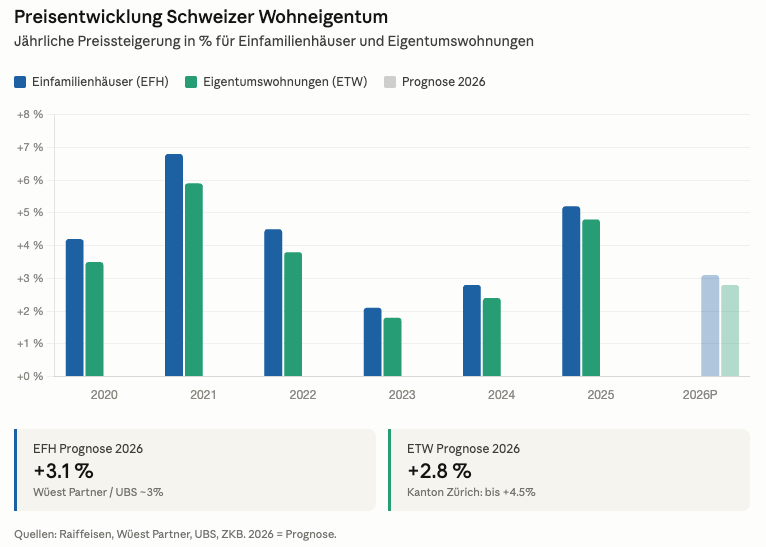

The figures speak for themselves: in the first quarter of 2026, prices for detached houses in Switzerland rose by an average of 1.4 per cent compared with the previous quarter, and for owner-occupied flats by as much as 1.8 per cent. On an annual basis, this results in an overall increase of around 5.2 per cent for residential property – the sharpest rise in over three years. For 2026 as a whole, Wüest Partner forecasts a value increase of around 3.1 per cent for detached houses and 2.8 per cent for flats; UBS also expects a rise in value of around 3 per cent.

Demand is particularly strong in established locations. In the canton of Zurich, Zürcher Kantonalbank expects price rises of around 4.5 per cent. Thanks to international demand, Geneva remains a distinct market with its own dynamics. The limited supply – hardly any new-builds in Zurich, structural shortages in Geneva – is driving prices in the premium segment disproportionately higher. Anyone who owns a high-quality, owner-occupied property is in one of the most sought-after spots on the European property market – and anyone wishing to acquire one should not wait too much longer.

The interest rate environment: a historic advantage that won’t last forever

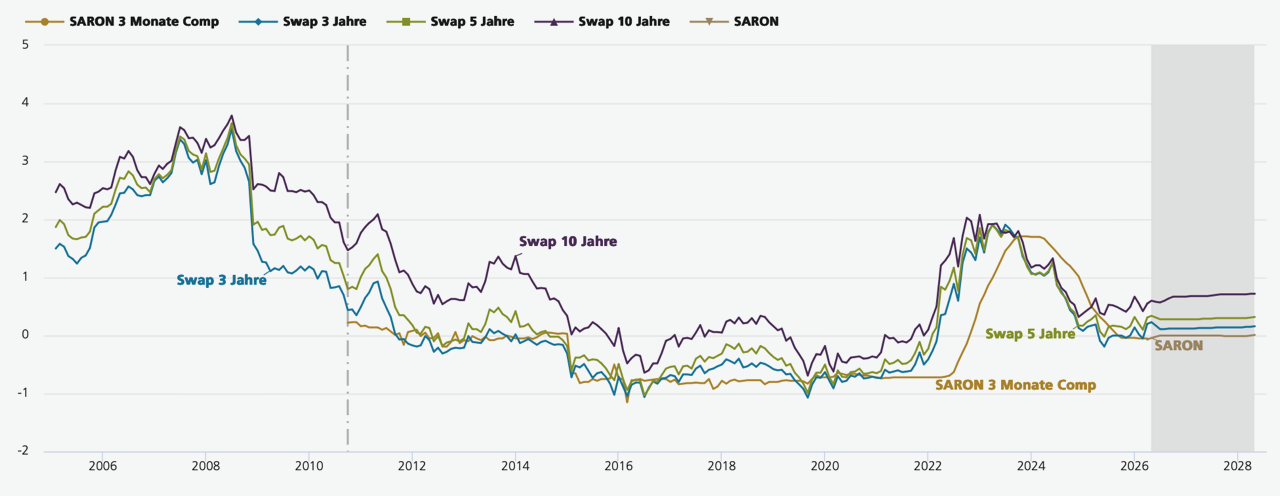

The exceptionally low interest rates are a major factor in this development. The Swiss National Bank has gradually lowered its key interest rate to zero per cent by June 2025 and is likely to maintain this level throughout 2026. The inflation rate stands at just around 0.3 per cent – well within the SNB’s target range – and economic growth remains moderate, with forecasts of 0.9 to 1.3 per cent.

What does this mean in practical terms for property buyers? Five-year fixed-rate mortgages are currently available from around 1.2 per cent, and ten-year mortgages from around 1.5 to 1.9 per cent. SARON mortgages are at historic lows. UBS forecasts that mortgage rates will remain within the current range over the coming quarters – without a further decline, but also without a significant rise. The first interest rate rises are expected in the first half of 2027 at the earliest, should the economic situation in Europe improve.

This presents a clear opportunity for property buyers: Anyone taking out a long-term fixed-rate mortgage today secures the current rate and protects themselves against the foreseeable rise in interest rates from 2027 onwards. Affordability remains – despite higher prices – at a historically comparatively favourable level. However: Household debt is already rising more sharply than incomes, which UBS notes as a worrying sign in its Swiss Real Estate Bubble Index.

Bubble risk is rising – but the market is holding up (for now)

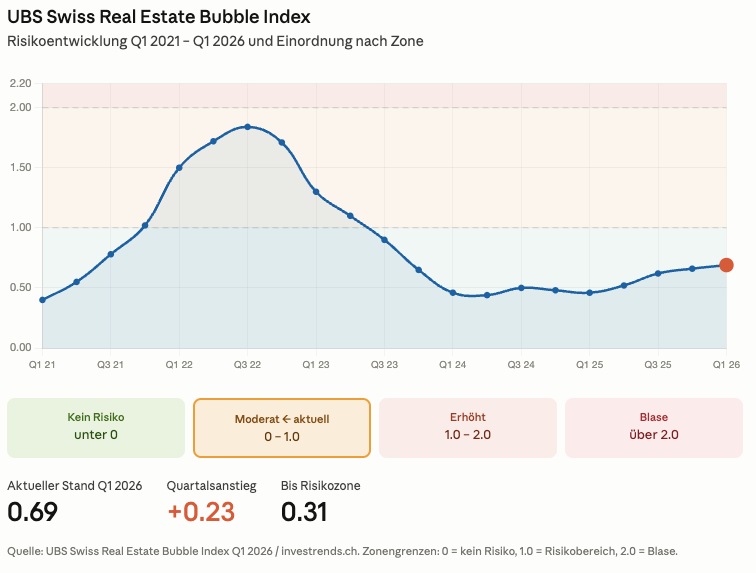

The UBS Swiss Real Estate Bubble Index PDF download climbed to 0.69 index points in the first quarter of 2026 – an increase of 0.23 points. The risk zone begins at 1.0 points, with an actual bubble defined as 2.0 points or above. The market is therefore still in the ‘moderate’ risk zone, but the trend is clearly upwards; the rise in the previous quarter was the strongest since 1989.

Zero interest rates and a subdued economy are the driving forces behind this rise. For owners of exclusive properties, this signal is a double-edged sword: on the one hand, it reflects persistently high demand and confirms the value of their property. On the other hand, it calls for vigilance – because what rises quickly can also correct if the interest rate environment shifts or the economy slumps.

Political risks: Growing regulatory pressure

Alongside the economic environment, a factor that has long been underestimated is coming to the fore: political intervention in the housing market. In the canton of Zurich, several key housing policy decisions are due in 2026 that could fundamentally alter the market environment. The Housing Protection Initiative provides that municipalities may introduce far-reaching measures if the vacancy rate falls below 1.5 per cent – including permit requirements for conversions, demolitions and the conversion of rental properties into freehold ownership, as well as temporary rent caps.

As this threshold has long been undershot in Zurich, Winterthur and many other cities, such regulations would have immediate consequences. Legal experts warn of a ‘patchwork’ of differing municipal regulations, leading to considerable planning uncertainty. At federal level, the Tenants’ Association is collecting signatures for a rent initiative that would provide for a systematic and regular review of all rents.

For owners of owner-occupied premium properties, these developments are less directly relevant than for yield investors. Nevertheless, regulatory uncertainties have a dampening effect on development potential and thus indirectly on valuations – as institutional investors are already factoring into their acquisition calculations.

What this means for sellers: Seize the window of opportunity

For owners considering a sale, experts paint a clear picture: the current moment is exceptionally favourable. The combination of high market prices, low interest rates (which keep a relatively broad group of buyers financially viable) and robust demand creates optimal selling conditions. The UBS Real Estate Bubble Index explicitly describes the situation for homeowners looking to sell as ‘very comfortable’.

In the exclusive segment, there is the added factor that high-quality, well-located properties remain in short supply. Buyers with the necessary funds are competing for a limited supply – which strengthens sellers’ negotiating position. Anyone planning a forthcoming life stage that is conceivable without owning their own property – succession planning, inheritance, consolidation of assets – should not lightly let the current window of opportunity go to waste.

What this means for buyers: Decide before conditions change

For owners looking to buy – whether first-time buyers in the premium segment or those wishing to upgrade or move – the following applies: Interest rates are expected to remain favourable until the end of 2026, after which the likelihood of higher financing costs increases. Those who buy today and secure a long-term fixed-rate mortgage stand to benefit twice over: from terms that are still affordable at present and from a market that offers further potential for appreciation in the medium term.

The crucial question is not whether the market will turn – but when. For owner-occupied properties in prime locations, history has shown that long-term holding strategies are rewarded above average. The demographic fundamentals, the structural supply shortage and the stability of Switzerland as a business location point to a solid foundation under prices – even if a correction were to bring about short-term adjustments.

Conclusion: Acting strategically in an extraordinary market moment

The Swiss market for exclusive residential properties finds itself in an unusual state of tension: record prices meet historically low interest rates, strong fundamentals meet growing political risks, and sustained demand meets the first signs of saturation in the luxury segment. This constellation demands one thing from both buyers and sellers: strategic clarity.

Those looking to sell have rarely encountered more favourable conditions. Those looking to buy should take advantage of the interest rate window before it begins to close from 2027 onwards. And those who wait risk finding that conditions which seem ideal today will be a thing of the past tomorrow.

In a market environment characterised by contradictions, with enormous opportunities and risks shaped by global and local political developments, we at Wüst und Wüst advise our clients on the development of strategies and support them in their implementation. Thanks to our offices in Küsnacht/Zurich, Lucerne, Zug, St. Moritz, Zug, Pfäffikon/SZ and Basel, we possess comprehensive market knowledge and many years of experience. Thanks to our partnership with Christie’s International Real Estate, we also have a strong global network.

This article is based on data and analyses from the UBS Mortgage Rate Forecast May 2026, the NZZ Real Estate Newsletter May 2026 and current market reports from Wüest Partner, Raiffeisen and other sources.