SNB stays the course. Mortgage rates remain low.

23.03.2026The Swiss National Bank (SNB) has left its key interest rate unchanged at 0%. In a market environment characterised by global uncertainties, the central bank is thus sending a clear signal of continuity. For owners as well as prospective buyers of exclusive properties, this means one thing above all: a high degree of planning security with low mortgage rates.

A signal of reliability in turbulent times

Despite geopolitical tensions in the Middle East and fluctuating energy prices, the SNB remains true to its line in its monetary policy assessment of 19 March 2026. The decision to keep the key interest rate at 0% underlines the commitment to supporting the Swiss economy and keeping inflation within the target range of 0% to 2%.

This news is of great significance for the high-end property sector. Stable interest rates provide fertile ground for long-term investment. Anyone currently investing in prime locations or rebalancing their portfolio benefits from a predictable financing environment.

Focus on price stability and a strong franc

The SNB is closely monitoring the situation on the foreign exchange market. To counteract an excessive appreciation of the Swiss franc – often sought as a “safe haven” in times of crisis – the National Bank is prepared to intervene actively. The SNB’s monetary policy thus helps to keep inflation within the price stability range and supports economic development. This policy not only protects the export economy but also preserves the value of tangible assets within Switzerland. For international buyers, the Swiss property market therefore remains one of the most attractive and secure destinations worldwide.

Outlook: Moderate growth and low inflation

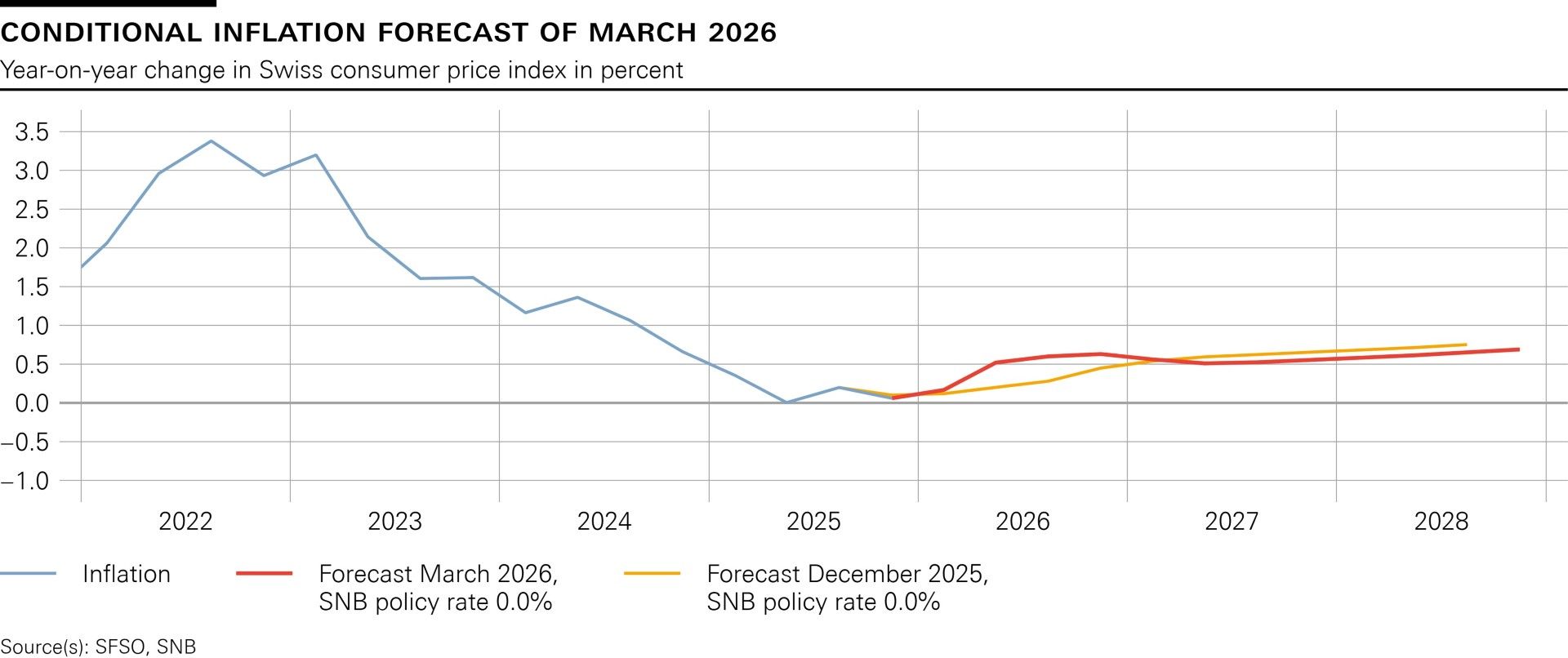

The SNB’s forecasts paint a picture of cautious optimism: in terms of economic growth, the National Bank expects GDP growth of around 1% in 2026, which is likely to accelerate to 1.5% in 2027. According to the bank, inflation will continue to hover between 0.5% and 0.6% until 2028. The forecast is based on the assumption that the SNB’s key interest rate will remain at 0% throughout the forecast period.

Although energy prices are expected to rise slightly in the short term, medium-term pressure remains stable. This creates an environment in which luxury properties serve not only as a well-maintained living environment but also as a hedge against global currency risks.

Forecast not without caveats

Despite the high probability of the forecasts published by the SNB regarding Swiss economic development, it also points to the current high risks. It writes: “The outlook for the global economy is subject to significant risks, particularly due to the situation in the Middle East. Energy prices could therefore rise more sharply than expected in the baseline scenario, which would significantly increase inflation and noticeably slow economic growth. Potential supply chain issues and increased uncertainty could also weigh on growth. In addition to the situation in the Middle East, the outlook for trade policy also remains uncertain.”

Stable conditions expected until 2028

The SNB’s decision is a commitment to Swiss stability. Whilst other currency areas are grappling with more volatile inflation rates, Switzerland offers a calm environment. For buyers and sellers in the luxury segment, this means that the conditions for transactions remain extremely attractive. Property assets in prime locations are and will remain the gold of the Swiss economy.

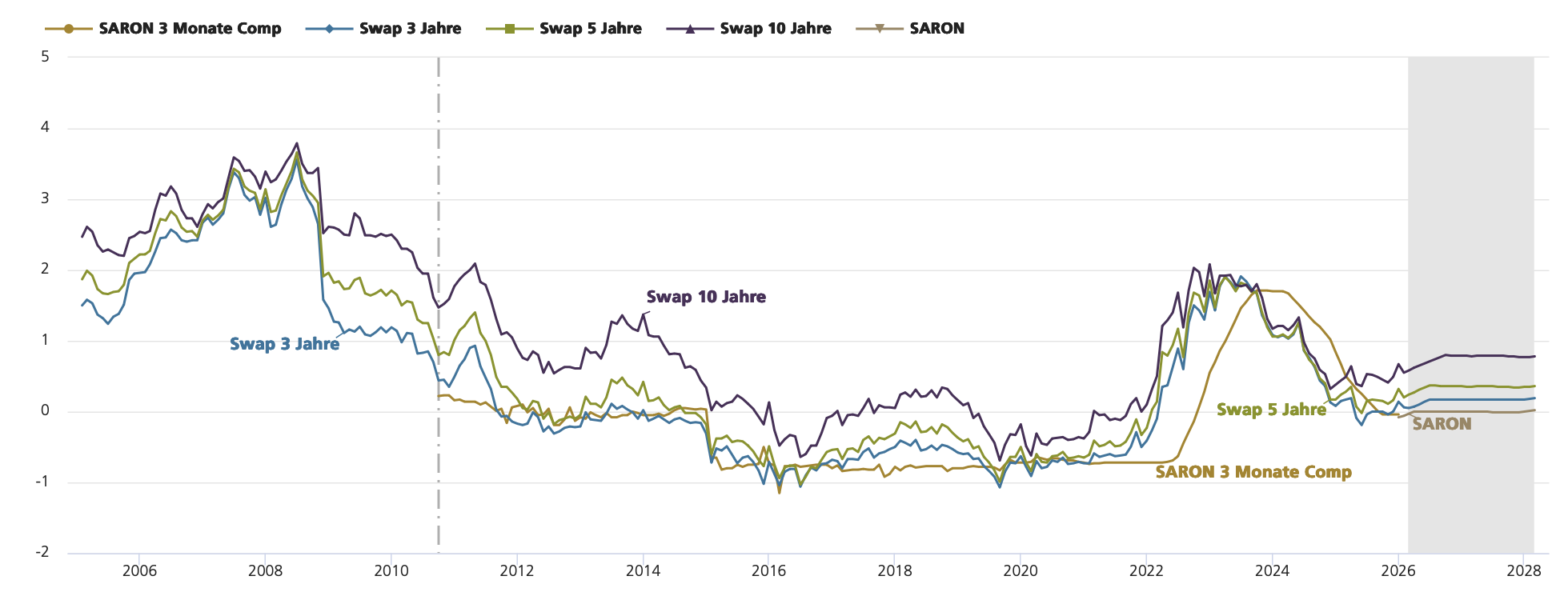

UBS expects interest rates to remain low

UBS also anticipates that interest rates will remain low in its latest interest rate forecast. However, the bank notes that the conflict with Iran is overshadowing the SNB’s assessment of the situation. Nevertheless, it shares the SNB’s view and does not expect any change in monetary policy over the next twelve months. “As long as the SNB sticks to its zero interest rate policy, interest rates are likely to remain very low by historical standards. SARON-based mortgage rates are likely to move sideways.” (Quote from UBS)